")

Subscribe

Introduction and investment thesis

Most recently I wrote about Twilio (NYSE: TWLO) in July, where I raised my rating on the stock from “Hold” to “Buy” as I believed that the company was showing early signs of stabilization after the Management conducted a business review of its segment business and laid out its long-term success plan. Although revenue growth had not accelerated at the time of my writing, there were early signs of stabilization in the net retention rate. Since then, the stock has outperformed the index, gaining 6% in the previous month while the S&P 500 had fallen 5%.

The company recently reported its results for the second quarter of fiscal 2024. Revenue and non-GAAP operating income increased 4% and 45% year-over-year, respectively, beating estimates. During the quarter, Twilio continued to implement targeted go-to-market strategies to acquire and cross-sell in larger deals by expanding the network of partners and ISVs and implementing robust product innovations in both the communications and segment business. What I would also like to note is that losses in the segment business are narrowing, which I think is a positive sign. Finally, management has also sound The company is optimistic about its outlook and overall business strategy and has raised its revenue and earnings expectations for the third quarter.

While the company has yet to see a significant acceleration in revenue growth, I believe management’s focus on product innovation and financial discipline to bring stability to the company is a step in the right direction. Looking at both the “good” and “bad” aspects, I believe Twilio remains a “buy” with a $95 price target.

The communications business is stabilizing, while the segment business is showing signs of improvement

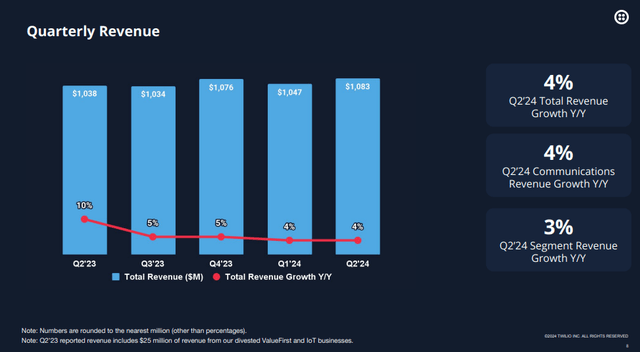

Twilio reported its results for Q2 of fiscal 2024. Revenue grew 4% year-over-year to $1.083 billion, beating estimates. Active customer accounts grew nearly 4% to 316,000. Of the $1.083 billion in revenue, the communications business grew 4% year-over-year to $1 billion, contributing 92.5% of total revenue, while segment business grew 3% (slightly faster than the previous quarter) to $75 million, contributing the remaining 7.5% of total revenue. During the quarter, the company continued to drive its business with increasing rigor, as evidenced by its go-to-market strategies as well as robust product innovations, combining its communications capabilities, AI and rich contextual data to help companies deliver more personalized interactions with their customers throughout their customer journey while achieving faster time to value.

Results review Q2 FY24: Stabilizing sales growth

In the communications business, Twilio continues to expand its network of partners and ISVs to win and sell larger contracts across geographies and industries. At the same time, the company also saw greater adoption of its higher-margin AI products such as Verify and Voice Intelligence, where customers are seeing higher response rates and productivity gains.

Regarding its Segment business, Twilio continued to focus on increasing its go-to-market efficiency, resulting in a significant increase in the number of multi-year contracts, from 17% of new bookings in Q2 FY23 to 40% of new bookings in Q2 FY24. In my previous post, I discussed that Twilio has been focused on building better synergies between its Communications and Segment products, and this quarter launched a personalized virtual agent in private beta that natively embeds Segment into Communications and allows customers to receive interactive and personalized voice responses, while also releasing Data Graph and Linked Audiences, which allow companies to combine centralized data, AI, and real-time events to create ideal customer profiles for better customer engagement.

Increasing profitability by reducing losses in segment business

Twilio shifted gears toward profitability, generating non-GAAP operating income of $175 million, up over 45% year-over-year, with margin improvement of 460 basis points to 16.2%. Similar to previous quarters, the Communications business did the bulk of the work, generating non-GAAP operating income of $250 million with a margin of 24.8%, while the Segment Business generated a loss of $16 million with a margin of -21%.

However, I would like to note that the non-GAAP operating loss from the segment business has started to narrow sequentially, demonstrating management’s commitment to making its segment business profitable (on a non-GAAP basis) by the second quarter of fiscal 2025. While the company is pursuing more efficient go-to-market strategies to acquire larger customers and effectively cross-sell to increase customer lifetime value, it has simultaneously rationalized its operating expenses, particularly sales and marketing, which represented 15.9% of total revenue in the second quarter of fiscal 2024, compared to 19.1% in the second quarter of fiscal 2023.

Net dollar retention rate declines year-on-year but shows signs of sequential stabilization

In my previous posts, I explained that Twilio’s revenue growth slowed while net retention rate plummeted due to a challenging macroeconomic environment with constrained budgets from existing and new customers, resulting in lower usage of their products or lower contract values. Over the last two quarters, we observed a decline in net retention rate year-over-year, but on a sequential basis, there were signs of stabilization as management conducted a business review of its segment business to address glaring underperformance and laid out its plan for long-term success, which emphasized investing in targeted R&D spend to drive AI-driven product innovation while increasing profitability.

During this quarter’s earnings call, management outlined that it does not make plans for any macroeconomic environment, good or bad. While this statement is somewhat ambiguous, I believe that overall management is confident in its business strategy and forecasts. In the future, should the U.S. economy continue to weaken from its current levels or, worse, enter a recession, I believe the company could face renewed headwinds to its revenue growth. I believe investors have currently moved from “deep pessimism” to “cautious optimism” and expect Twilio to expand its current net retention rate as well as the contribution of large customer revenue to overall revenue growth.

Results review Q2 FY24: Stabilization of net retention rate

Review of my rating: The risk-reward ratio appears attractive.

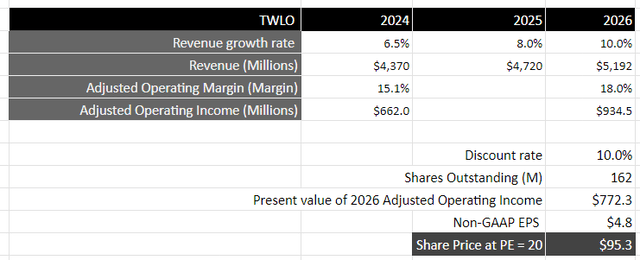

Looking ahead, management increased its third quarter revenue and earnings guidance by 3.3% and 17.8%, respectively (compared to previous guidance), to $1.09 billion and $165 million, respectively, while slightly reducing the range of its full-year 2024 revenue guidance to 6-7% (previously 5-10%) and increasing its estimate for non-GAAP operating income by 8.6% to $662 million.

Assuming the U.S. economy does not enter a deep recession, management should continue to execute on its business strategies by driving growth through targeted AI-driven product strategies to embed Segment natively into communications to accelerate time to value for its customers. In that case, I believe the company should return to high-single-digit to low-double-digit revenue growth, driving revenue of approximately $5.2 billion by fiscal 2026.

From a profitability perspective, assuming Twilio can increase its non-GAAP operating margin from a projected 15.1% to 18% over the next two years through the closing of larger deals and effective cross-selling, it should generate non-GAAP operating income of just under $934 million, which equates to a present value of $772 million at a 10% discount rate.

Using the S&P 500 as a benchmark, where companies grow earnings by an average of 8% over a 10-year period and whose price-to-earnings ratio is between 15 and 18, I believe that given the rate of earnings growth over that period, it should trade at least at par or 1.25x multiple, which equates to a P/E of 20 or a price target of $95, which represents 58% upside from current levels.

Author’s evaluation model

My final verdict and conclusions

In my previous post, I had upgraded my rating on the stock from Hold to Buy as I believed the company could be at an inflection point given its strategic initiatives to drive growth through targeted AI-driven product innovations while increasing profitability. From the latest earnings report, it is clear that the company is indeed seeing signs of stabilizing revenue growth, with its segment business slowly gaining traction as it pursues effective go-to-market strategies to win larger orders and multi-year contracts. At the same time, the company continues to see its profit margin expansion, with losses in the segment business narrowing as per management’s commitment, while net retention rates have stabilized. Finally, management also sounds increasingly optimistic about the direction of its business as it raised its revenue and earnings guidance for the third quarter. Although revenue has yet to pick up in any meaningful way and the company could face headwinds in the near term if the U.S. economy continues to weaken, I think the risk/reward proposition is attractive to take a position in the company, so I maintain my Buy rating but increase the price target to $95.