share: Uptrend due to put option sales")

JStudios

introduction

Bread Finance (NYSE: BFH), formerly known as Alliance Data Systems, is a consumer lender. Unlike rival OneMain Financial, Bread’s lending activities are primarily funded by depositors (like Synchrony Financial). Back in May, I wrote about the shares’ upside potential after they hit a 52-week high. Since then, shares have gained another 30%. Given such a rise and the risk of volatility in the broader market, I think it’s best to consider a cash-hedged put trade to generate income and an option to buy shares at a lower price.

Bread Financial’s second quarter results

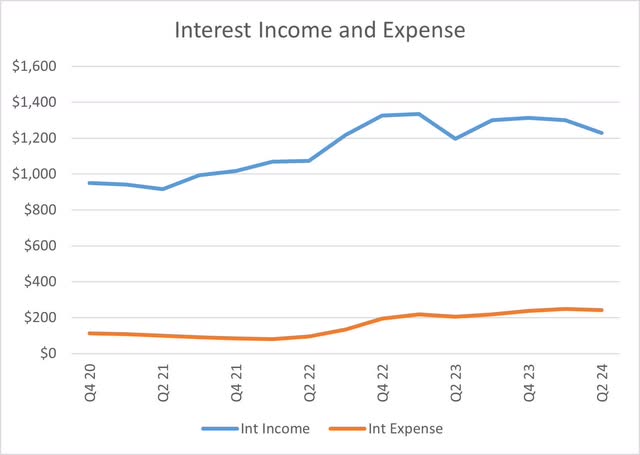

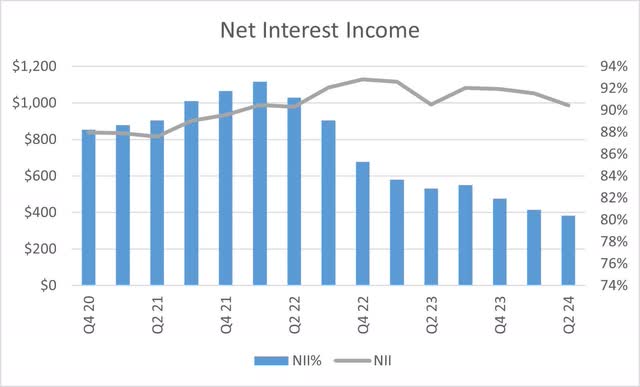

As with many banks, higher interest rates also increased Bread Financial’s borrowing costs. Fortunately, due to their positioning as a consumer lender, they have wide interest rate spreads. Interest income fell significantly in the second quarter, while interest expenses fell slightly. This led to a decline in net interest income (interest income less interest expenses), although this remains above the 2021 level.

Corporate Finance Corporate Finance

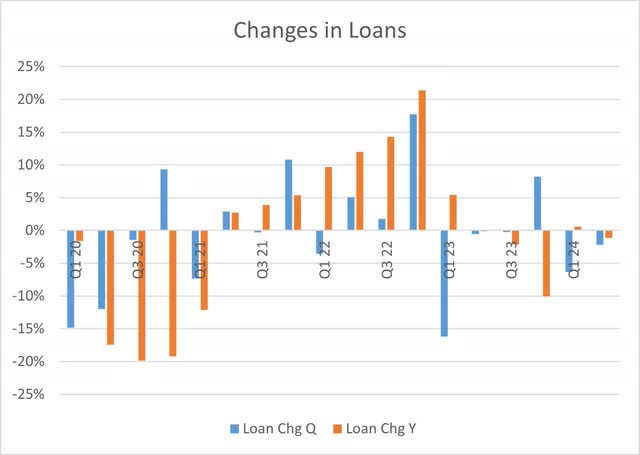

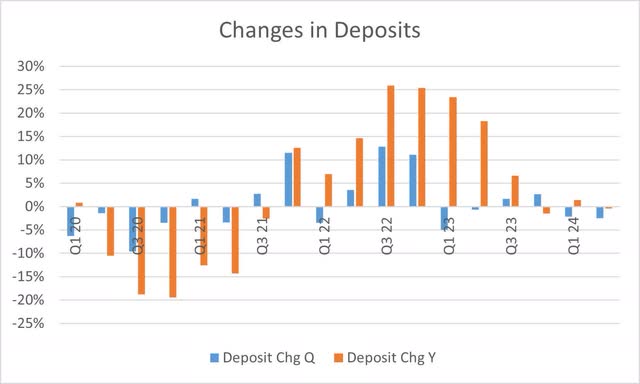

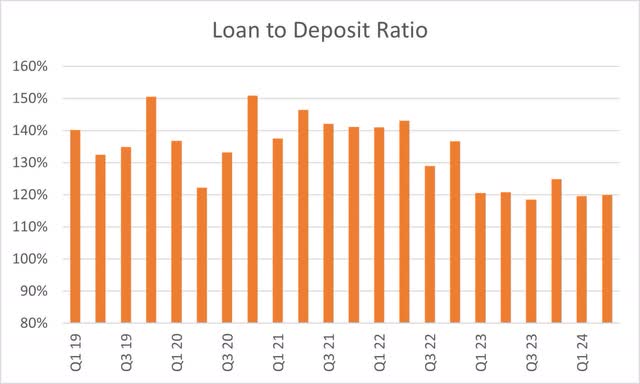

One of the reasons for the decline in net interest income was weak loan demand. The company’s loan balances declined for the second quarter in a row. Deposit activity also declined slightly more than lending in the second quarter, leading to an increase in the loan-to-deposit ratio to 120%. This is a high ratio and shows that Bread Financial relies on external debt to fuel loan growth. External debt tends to be more expensive than deposits, but high asset returns allow Bread Financial to absorb these costs.

Corporate Finance Corporate Finance Corporate Finance

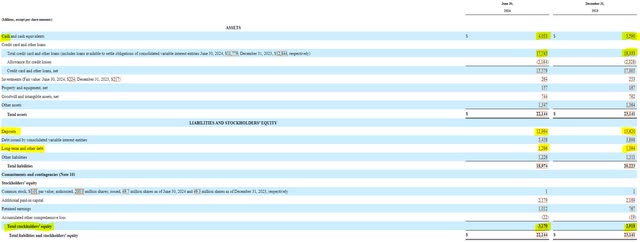

Despite relying on long-term debt to fund loan growth, Bread Financial has paid down its debt by $100 million to just under $1.2 billion in 2024. The company has also built over $4 billion in cash on hand and increased equity from $2.9 billion to $3.1 billion. The cash flow statement shows a little more detail. Bread Financial took in $924 million in cash from operations, plus $800 million from loan sales and repayments. They took the $1.7 billion in new cash and used it to cover the $627 million decline in deposits, plus debt reduction and a contribution to their consolidated variable rate unit. After that, the company put the remaining $500 million in the bank.

SEC10-Q

Risks for Bread Financial

Because of its position as a consumer lender, Bread Financial is vulnerable to economic fluctuations. Higher unemployment and/or lower wage growth lead to lower consumer spending and potential loan defaults. To date, Bread Financial has managed these risks well and loan defaults have decreased by nearly $200 million (less than $1 billion) compared to the end of last year.

SEC10-Q

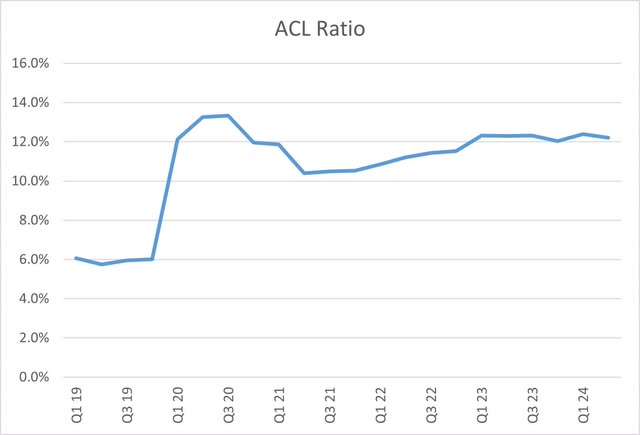

In addition to its manageable delinquencies, Bread Financial has set aside a loan loss provision to absorb any increase in loan defaults. Before the pandemic, Bread’s loss provision was only 6% of gross loans, but since then it has doubled to over 12%. In the event of loan write-offs, the company is well positioned to absorb those losses.

Corporate Finance

An income-based trade you should consider

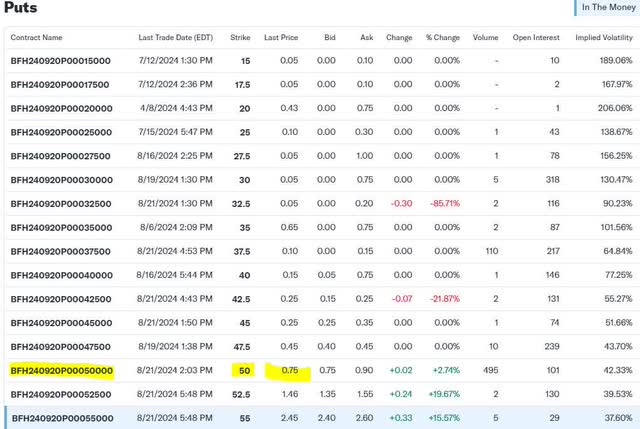

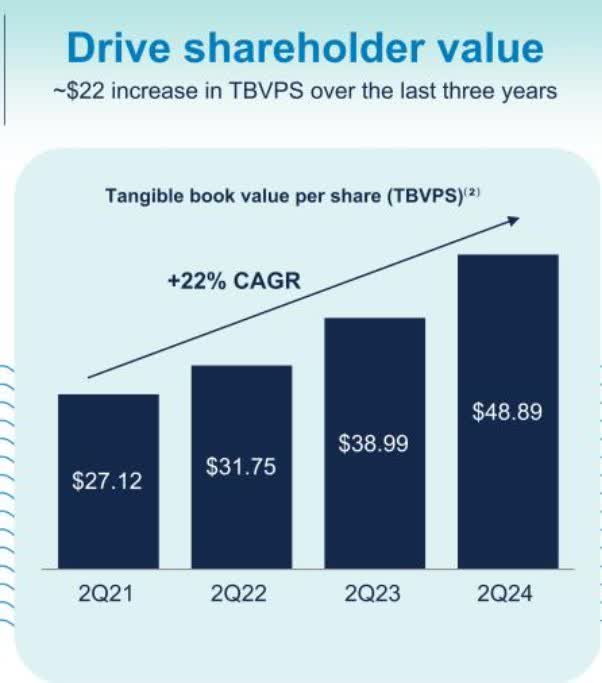

While I’m not a fan of buying shares at these levels, I believe a sell-off would provide a good entry point for investors. Therefore, I’m a fan of selling cash-backed puts with a strike price of $50 per share. Yesterday, these options traded at 75 cents per share, representing an 18% annualized return. If shares continue to stay high, simply collect the premiums and enter into a new contract for another round of income when the trade expires. I believe $50 per share is a good entry point because it’s roughly in line with current tangible book value, which management has done an excellent job of increasing over the past three years.

Yahoo Finance Presentation of results

Diploma

Bread Financial is in the volatile consumer lending business. While the economic outlook has worsened and consumer spending could decline, Bread Financial’s management has set aside a strong loan loss provision to offset a rise in the company’s delinquencies. In addition, the increased tangible book value per share underscores the underlying value that has been created. With shares rising so quickly in recent months, cash-backed puts are the best option to secure entry at a lower price while still collecting income.