")

The (TWSE:4572) was strong after the company recently reported solid earnings, but we believe shareholders may be missing some concerning details in the numbers.

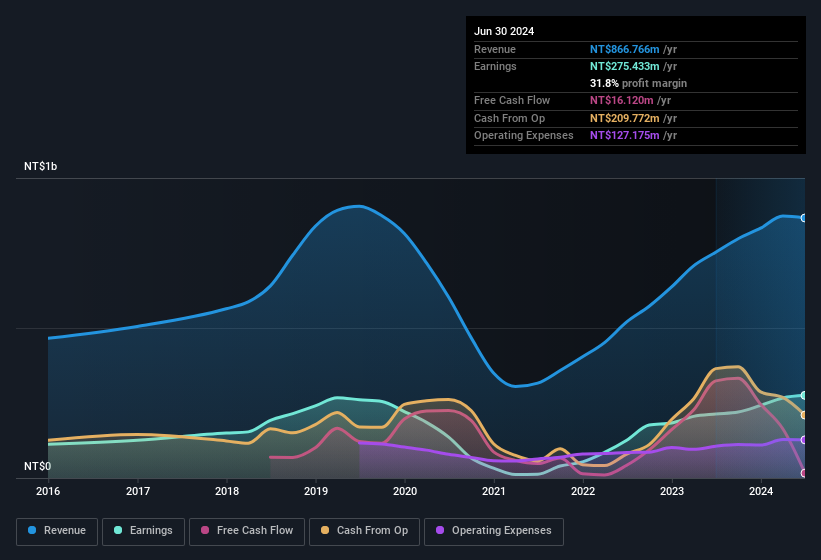

Check out our latest analysis for Drewloong Precision

Zoom in on Drewloong Precision earnings

An important financial metric that measures how well a company converts its profit into free cash flow (FCF) is the Delimitation ratio. To get the accrual ratio, we first subtract FCF from profit for a period and then divide that number by average funds from operations for the period. This ratio indicates how much of a company’s profit is not covered by free cash flow.

This means that a negative accrual ratio is a good thing because it shows that the company is generating more free cash flow than its earnings would suggest. This is not to say that we should be concerned about a positive accrual ratio, but it is worth noting when the accrual ratio is quite high. This is because some academic studies have pointed out that high accrual ratios tend to lead to lower earnings or lower earnings growth.

Drewloong Precision has an accrual ratio of 0.28 for the year to June 2024. We can therefore conclude that its free cash flow fell far short of covering its statutory profit, suggesting we should think twice before giving the latter much weight. In fact, the company reported free cash flow of NT$16m over the last twelve months, which is considerably lower than its profit of NT$275.4m. Drewloong Precision’s free cash flow actually declined last year, but it could recover next year as free cash flow is often more volatile than accounting profit. The good news for shareholders is that Drewloong Precision’s accrual ratio was much better last year, so the poor reading this year could simply be due to a short-term mismatch between profit and FCF. As a result, some shareholders may be hoping for stronger cash conversion in the current year.

You may be wondering what analysts are predicting in terms of future profitability. Fortunately, you can click here to see an interactive chart depicting future profitability based on their estimates.

Our assessment of Drewloong Precision’s earnings development

Drewloong Precision’s accrual ratio for the trailing twelve months shows that its cash conversion is less than ideal, which negatively impacts our view of its earnings. For this reason, we believe Drewloong Precision’s statutory profits could be better than its underlying earnings power. However, the good news is that its EPS growth over the past three years has been very impressive. Ultimately, it’s important to consider more than just the factors mentioned above if you want to properly understand the company. If you want to dive deeper into Drewloong Precision, you should also investigate what risks it is currently facing. Our analysis shows 2 warning signs for Drewloong Precision (1 is significant!) and we strongly recommend you look at them before investing.

Today we’ve focused on a single data point to better understand the nature of Drewloong Precision’s profit. But there’s always more to discover if you’re able to dig deeper. Some people consider a high return on equity to be a good sign of a quality company. Although this may require a little research, you may find that free Collection of companies with high return on equity or this list of stocks with significant insider holdings may prove useful.

New: Manage all your stock portfolios in one place

We have the the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of portfolios and see your total amount in one currency

• Be notified of new warning signals or risks by email or mobile phone

• Track the fair value of your stocks

Try a demo portfolio for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.

are privately owned, 36% are owned by private investors.")