")

Last week’s earnings announcement from Fabasoft AG (ETR:FAA) was disappointing for investors despite strong headlines. We believe the market may be paying attention to some underlying factors that it finds concerning.

Check out our latest analysis for Fabasoft

Fabasoft’s earnings in detail

In high finance, the most important metric that measures how well a company converts reported earnings into free cash flow (FCF) is the Delimitation ratio (from cash flow). To get the accrual ratio, we first subtract FCF from profit for a period and then divide that number by the average funds from operations for the period. The ratio tells us how much a company’s profit exceeds its FCF.

This means that a negative accrual ratio is a good thing because it shows that the company is generating more free cash flow than its earnings would suggest. While an accrual ratio above zero is of little concern, we think it is noteworthy when a company has a relatively high accrual ratio. In particular, there is some academic evidence to suggest that a high accrual ratio is generally a bad sign for near-term earnings.

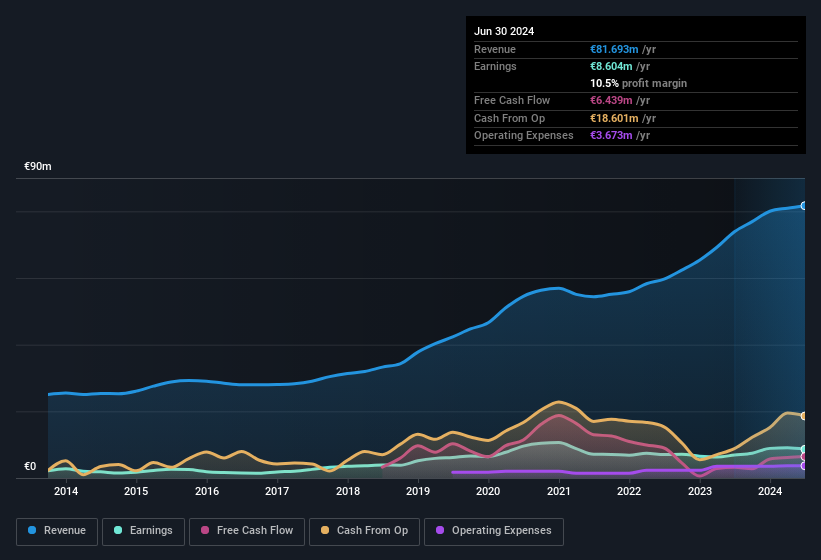

In the twelve months to June 2024, Fabasoft recorded an accrual ratio of 0.40. Ergo, its free cash flow is significantly weaker than its profit. Statistically speaking, this is a real disadvantage for future profits. This means that Fabasoft generated free cash flow of €6.4 million during this period, which was well below the reported profit of €8.60 million. However, we would like to point out that Fabasoft has increased its free cash flow over the past year.

You may be wondering what analysts are predicting in terms of future profitability. Fortunately, you can click here to see an interactive chart depicting future profitability based on their estimates.

Our assessment of Fabasoft’s profit development

As we’ve already made clear, we’re a little concerned that Fabasoft was unable to back up last year’s profit with free cash flow. For this reason, we believe Fabasoft’s statutory profits may be a poor indicator of underlying earnings power and give investors an overly positive impression of the company. Still, it’s worth noting that earnings per share have grown by 23% over the past three years. Of course, we’ve only scratched the surface when analyzing profit; one could also consider margins, forecast growth and return on capital, among other things. If you want to dive deeper into Fabasoft, you should also examine what risks the company is currently facing. For example, we found out 1 warning sign which you should definitely take a look at in order to get a better idea of Fabasoft.

Today we have focused on a single data point to better understand the nature of Fabasoft’s earnings. But there are many other ways to form an opinion about a company. For example, many people consider a high return on equity to be an indication of a favorable business situation, while others like to “follow the money” and look for stocks that insiders are buying. Although this may require a little research, you may find that free Collection of companies with high return on equity or this list of stocks with significant insider holdings may prove useful.

New: AI Stock Screeners and Alerts

Our new AI Stock Screener scans the market daily to uncover opportunities.

• Dividend powerhouses (3%+ yield)

• Undervalued small caps with insider purchases

• Fast-growing technology and AI companies

Or create your own from over 50 metrics.

Try it now for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.