yet")

Image source

A bank that I am fairly neutral towards is East West Bancorp (NASDAQ:EWBC). For those who don’t know the institution, it is a fairly large player in the financial sector with a market capitalization of This letter contains $10.69 billion. While there are many other banks larger than it, this is one of the larger ones I’ve analyzed. And as you can imagine, an institution of this size has a significant reach. And the reach extends not only to parts of the U.S. like California, Texas, and New York, but also to parts of Asia like China and Singapore.

From an asset quality perspective, East West Bancorp is a fairly robust institution. In addition, the company is valued quite attractively, at least relative to earnings. But on a price-to-book basis and relative to book value, the shares are a little high. Revenue and earnings have been a little disappointing recently, even though the bank’s noninterest income has been rising. And when you add to that how the shares are valued on a book value basis, I don’t think I’m ready to upgrade it from Hold. I had it when I last wrote about it not yet declared a ‘buy’ in December 2023.

Growth continues

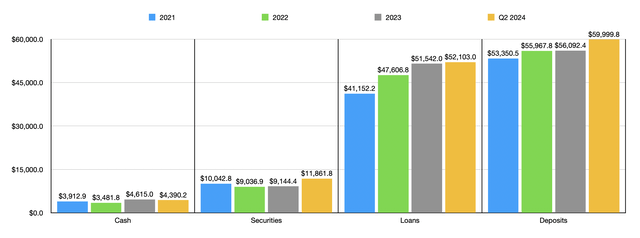

When it comes to the balance sheet, East West Bancorp is an interesting and growing company. At the end of 2023, for example, the bank had $56.09 billion in deposits on its books. These have grown since then, reaching $60 billion in the second quarter of fiscal 2024. This is not the only part of the balance sheet that has grown. The value of loans, for example, increased from $51.54 billion to $52.10 billion. And even more impressive growth can be seen when looking at securities. These amounted to $9.14 billion last year. But today they are a whopping $11.86 billion. And the company managed to do this while only experiencing a modest decline in cash, from $4.62 billion to $4.39 billion.

Author – SEC EDGAR Data

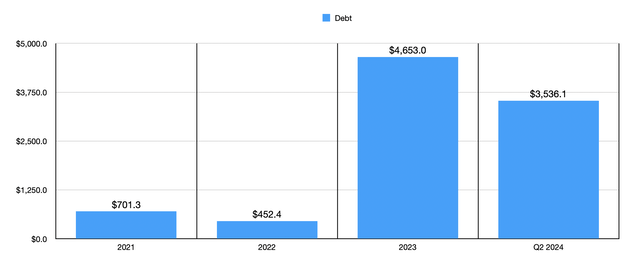

While it would have been nice if cash levels had increased as well, not everything can be perfect. And the good news is that that cash level has fallen in part because management has prioritized debt repayment. At the end of last year, total debt on the institution’s books was $4.65 billion. But by the end of the last quarter, that number had dropped significantly to $3.54 billion. That’s still a far cry from its previous debt levels. At the end of 2022, for example, the company only had $452.4 million in debt on its books. But due to the banking crisis, many banks decided to increase their debt levels to bolster their balance sheets with fresh cash. And for a company that still has a fairly high risk of uninsured deposits at 42%, maintaining sufficient liquidity is important to avoid the appearance of trouble should times get tough again.

Author – SEC EDGAR Data

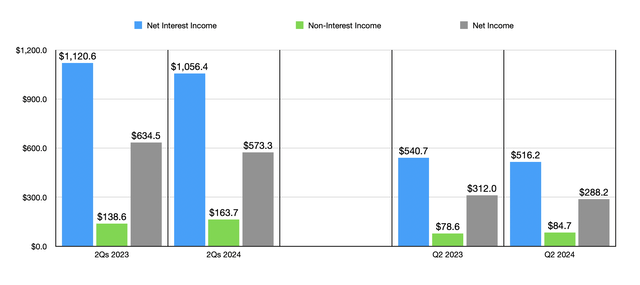

As for the income statement, the picture was disappointing all around. Last quarter, net interest income was $516.2 million, down from the $540.7 million reported a year earlier. An increase in interest-bearing liabilities as well as a slight decline in the company’s net interest margin from 3.34% to 3.27% are largely responsible for this. But even when comparing the first half of this year with the same period last year, it is clear that the decline from $1.12 billion to $1.06 billion, which was due not only to an increase in interest-bearing liabilities but also to a decline in the net interest margin from 3.55% to 3.27%, is part of a recent trend.

Author – SEC EDGAR Data

Fortunately, the bank’s noninterest income has been rising while net interest income has come under pressure. For the first half of this year, the company reported noninterest income of $163.7 million. That’s a significant increase from the $138.6 million reported a year earlier. Higher fee income, largely due to growth in asset management fees charged by the company, as well as an increase in fees on deposit accounts and loans, can be blamed for much of that improvement. But that wasn’t enough to prevent net interest income from falling from $634.5 million last year to $573.3 million this year. And even in the most recent quarter, the $288.2 million reported by management was slightly below the $312 million recorded during the same period in 2023.

Author – SEC EDGAR Data

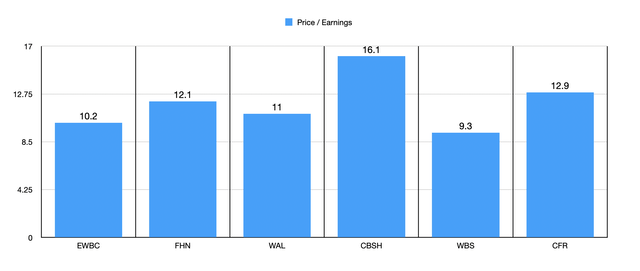

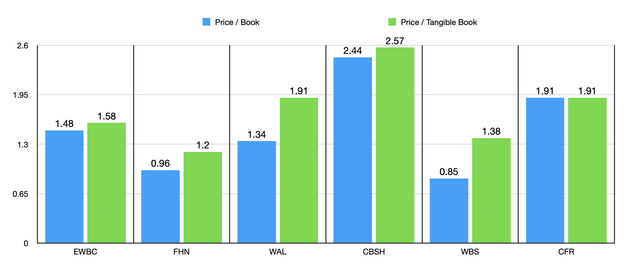

If we base our calculations on results from 2023 onwards, the company’s shares appear fairly valued at a price-to-earnings ratio of 9.2. However, if we annualize the 2024 data, we get a slightly higher value of 10.2. I typically prefer banks with price-to-earnings ratios between 6 and 10 times earnings, so this candidate is right at the high end of that range. In the chart above, you can see how this compares to five similar banks. Four of the five trade at price-to-earnings ratios higher than what East West Bancorp trades at. Of course, we can also value such an institution relative to book value and tangible book value. And in the chart below, I’ve done just that. On a price-to-book basis, three of the five companies I compared it to were trading lower than it is. And that number drops to two of the five if we use the price-to-book approach.

Author – SEC EDGAR Data

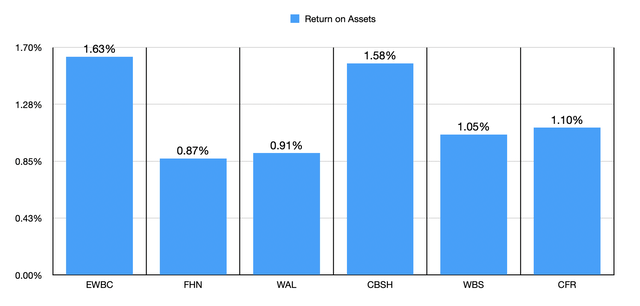

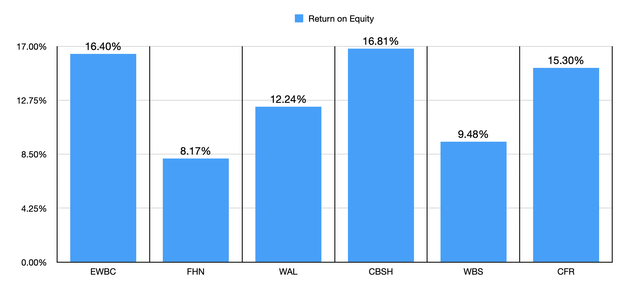

All of this places East West Bancorp more or less in the middle of the pack among its peers. However, some investors might argue that high asset quality justifies a premium. And it’s true that, at least on a relative basis, East West Bancorp has asset quality that’s at the higher end of the spectrum. In the chart below, I compared it to five companies using return on assets for each institution. And of all the companies, our candidate came in first. In the chart below, I did the same using return on equity. And in this scenario, the company’s 16.40% puts it above four of its five peers.

Author – SEC EDGAR Data

Author – SEC EDGAR Data

Take away

Such institutions are difficult for me to categorize. There are some very positive things about East West Bancorp that investors should note. Debt is coming down and most other parts of the balance sheet have improved. The shares are not overpriced, although they are certainly not the cheapest (except on a price-to-earnings basis). And asset quality appears to be quite high. We also have a high risk of uninsured deposits, which makes me a little uncomfortable. Add all of this together and you get a company that should probably fluctuate between “hold” and “buy.” But the value investor in me insists on having a fairly adequate margin of safety. And we don’t seem to have that in this case. So out of an overly cautious outlook, I think it makes the most sense to rate the company a “hold” at this point.

/cloudfront-us-east-1.images.arcpublishing.com/pmn/7N65ZDM5YFEKBMNSVJ5ZBNGYVQ.jpg "Black Girl Joy Bike Ride is for black women interested in easy, stress-free bike rides")