Andrew Harnik

Fed Chairman Jerome Powell gave his speech last Friday in Jackson Hole, Wyoming.

The essence of this speech is this:

“It is time to adjust the policy.”

“The direction of travel is clear, and the The timing and pace of rate cuts will depend on upcoming data, the evolving outlook and the allocation of risks.”

But Mr Powell finally warns us:

“The limits of our knowledge require humility and a critical mind, geared to learning from the past and applying it flexibly to our present challenges.”

The bottom line is that the Fed will begin to adjust its policy, but… and this is a very important “but”… we, the Fed, will work out that policy depending on… first… incoming data… second… the evolving outlook… and third… the allocation of risk.

Mr Powell, no matter what policy he advocated, always tried to err on one side one situation or another.

As Powell and the Fed sought to provide reserves to the banking system to combat the disruptions caused by the Covid-19 pandemic and the ensuing recession, Powell and the Fed continually sought to provide too many reserves to reduce the possibility of the economy spiraling even further into disaster.

While Powell and the Fed have been battling inflation for the past two years, Powell and the Fed have always tried to stay on the side of tightening monetary policy over a very long period of time. The Fed has been pursuing its quantitative tightening policy for 29 months.

By adopting a new stance, Mr Powell wants to ensure that he and the Fed do the right thing for a sufficiently long period of time.

That is why Mr Powell and the Fed will not immediately initiate a major cut in interest rates.

Mr Powell and the Fed will “feel their way” into the future.

But in the future, the Fed’s key interest rate is likely to fall.

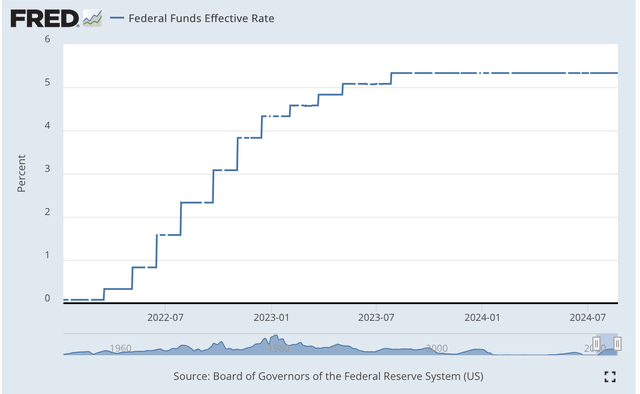

Here you can see how the Fed has raised the effective key interest rate over the past two years.

Effective interest rate for federal funds (Federal Reserve)

The last change in this key interest rate took place at the end of July 2023. This means that this key interest rate, effectively 5.33 percent, has existed for more than a year.

Fed policy consists of two parts: first, the actions taken and second, the “forecasts” that Federal Reserve officials give to the markets.

This approach has reduced investors’ inflation expectations for the next five to ten years to 2.1 percent for the time being.

The Fed’s actions in this part of the financial markets have apparently convinced investors that the Fed is serious about achieving its inflation target of 2.0 percent.

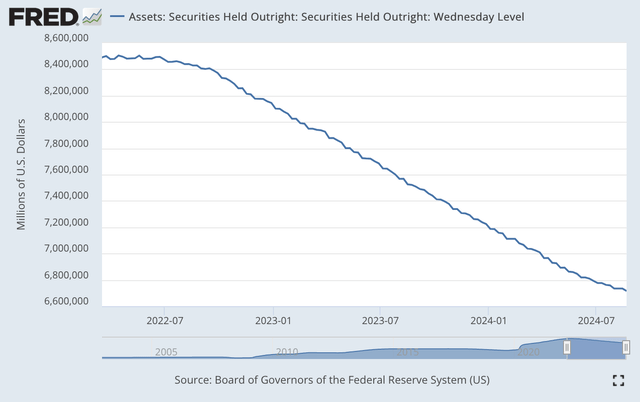

But that’s not all the Federal Reserve has done over the past twenty-nine months. It has also pursued a policy of quantitative tightening, working to reduce the size of the Fed’s securities portfolio.

Here is the Fed’s performance over the last twenty-nine months. The total reduction in the Federal Reserve portfolio was just under $1.8 trillion. As you can see, this reduction occurred in a very steady and sustained manner.

Fully held securities (Federal Reserve)

Since June, the Fed has reduced the amount of securities it allows to expire from its balance sheet.

Yet the Fed now has $3.0 trillion worth of securities in its portfolio, more than it had at the end of the period when it began pumping reserves into the banking system to combat the effects of the Covid-19 pandemic and the ensuing recession.

The question has always been when the Fed’s securities portfolio would return to a more “normal” level. Could Mr. Powell and the Federal Reserve introduce a “new” regime of “quantitative” policy as part of their “adjustment”?

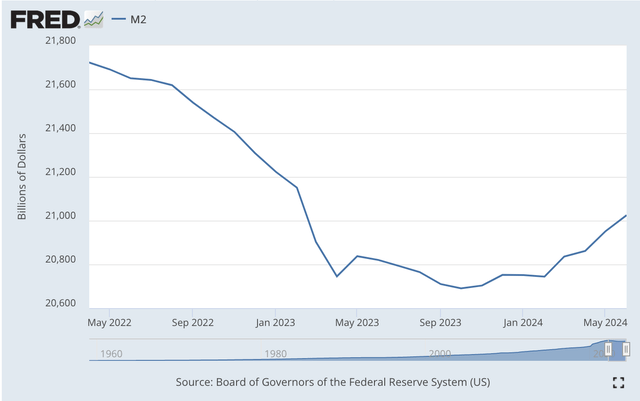

Then there is a third problem that is attracting analysts’ attention these days: concerns about the slowdown in the growth of the M2 money supply.

The M2 money supply has been declining since April 2022. The US economy has never experienced such a long period of monetary contraction without an economic recession occurring.

M2 money supply (Federal Reserve)

Economists and market participants are increasingly concerned about a possible recession in light of the measures taken by the US Federal Reserve.

As readers of my posts know, I am not overly concerned about this possibility since the Federal Reserve has pumped so much money into the economy in its efforts to combat the disruption caused by the Covid-19 pandemic and the ensuing recession.

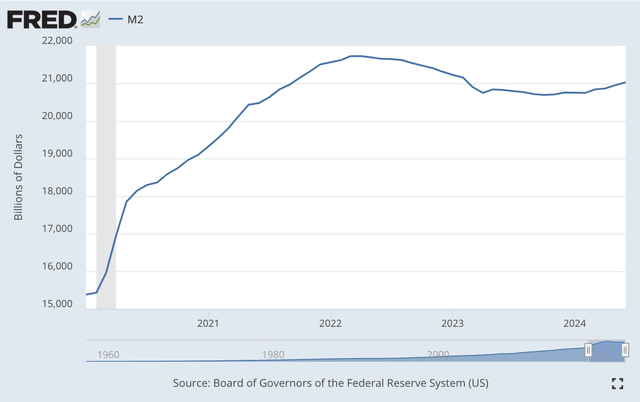

I think we need to add some earlier months to the table above.

M2 money supply (Federal Reserve)

In my opinion, this picture puts the current reduction in the M2 money supply into perspective.

The average annual growth rate of the money supply M2 is over 8.0 percent during this expansion phase.

From a historical perspective, the current situation can therefore be classified as “excessive” money supply growth.

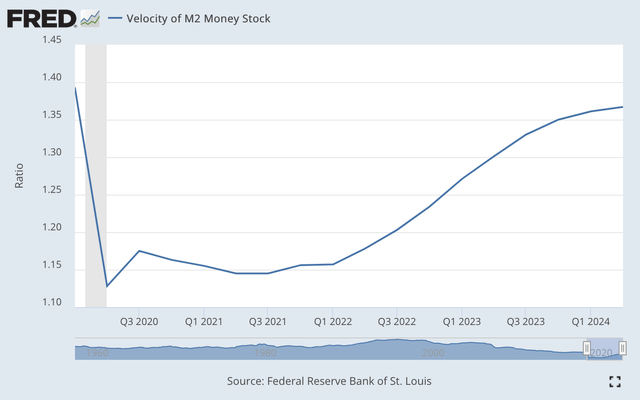

The only reason inflation did not get “out of control” is apparently because people were no longer using the money supply at the same rate as before. That is, the velocity of money decreased.

Velocity of money supply M2 (Federal Reserve)

Although the velocity of M2 money supply has increased, it has not yet returned to its previous level.

The result is that – as I have written many times – there is a lot of money “lying around” in the financial system.

For example, the commercial banking system has about $3.3 trillion in “vault money.”

This is one of the reasons why the US economy is still performing relatively well. And it is also the reason why the stock markets have reached all these “historic highs” while the Federal Reserve has been pursuing a policy of quantitative tightening.

In fact, in his speech in Jackson Hole, Mr. Powell gives an overview of the state of the economy and explains that it is doing relatively well.

Economic growth, Powell said, “continues…at a solid pace.”

“Prices have risen by 2.5 percent in the last twelve months.”

“The labor market has cooled significantly compared to its previous overheating.” This is the result of “a significant increase in the labor supply and a slowdown in the previously hectic pace of hiring.” It’s not that bad.

So the economy is doing quite well, but there are problems in the financial sector that need to be solved.

It is time for a policy adjustment.

But Powell reiterates that the Federal Reserve should not overdo it in its efforts to get everything right in the coming months.

The Federal Reserve will take action…but don’t expect them to act too quickly.