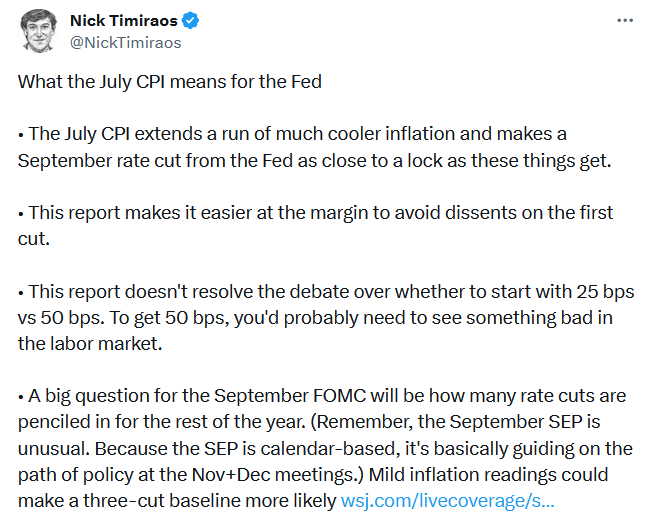

Unlike yesterday’s cooler-than-expected PPI report, the CPI was spot on. As expected, the CPI and CPI core rose 0.2% for the month. On an annual basis, they are 2.9% and 3.2%, respectively. The data pretty much set the Fed for a 25 basis point cut at the September meeting, as Nick Timiraos notes in his Tweet of the Day today. However, despite the CPI reading being as expected, the Fed may soon be worried about deflation if you look at the CPI without the protective pricing. Sound crazy?

Core CPI, excluding housing costs, was negative for the third month in a row. The last time it was negative for three months in a row was from March to May 2020, when the pandemic had shut down the global economy. CPI housing index is up 5.1% over the past year. Moreover, it accounts for 70% of the total core CPI value year-over-year. We have pointed out housing costs many times before. In summary, CPI housing costs, which make up 40% of CPI, are significantly lagging independent real-time market data and the Fed’s New Tenant Rent Index. When, not if, CPI housing costs catch up with market costs, 40% of CPI will head toward 0%. This will likely leave the Fed complaining about insufficient inflation or feared deflation.

Remember, we are not alone in this story. The Fed and most economists know that inflation excluding housing costs is below the Fed’s target. In addition, they are also aware of the flaws in the CPI data on housing costs.

What to watch today

revenue

Business

Market trading update

As noted yesterdayOne of the main market drivers is share buybacks, which quickly pick up after the end of the earnings season. These buybacks have contributed to a fairly strong market rally from the lows on Monday before last and triggered a short-term MACD. “Buy signal.”

While this bounce has been notable, the market is currently facing resistance at the 50-DMA and struggling to pull back from the July highs. If the market can overcome this resistance, a move towards 5600 becomes likely. However, given the magnitude of the move, we still suspect a slight retracement to the 100-DMA, which is likely to provide key support in the near term. A successful retest of this support would likely provide an entry point to slightly increase exposure in October. Remain cautious for now.

Google is in the crosshairs of the Justice Department

The Justice Department is considering various options for dealing with Google after winning its monopoly case against the company. One option being discussed is breaking up the company. Specifically, the company would then likely have to spin off its Android operating system. The Justice Department could take less drastic measures, such as forcing Google to share customer data with its competitors.

At the heart of the Google case are exclusive contracts. For example, Google pays Apple about $20 billion a year to make Google the default search engine on Apple devices. According to Evercore ISI, courtesy of Reuters:

“The most likely outcome now is that the judge rules that Google no longer has to pay for the default placement or that companies like Apple have to proactively ask users to choose their search engine rather than setting a default and allowing consumers to change the settings if they wish.”

Apple will also suffer if the Justice Department prohibits Google from entering into exclusive contracts. Reuters claims that the loss of Google’s $20 billion fee could negatively impact Apple’s earnings by 4-6%. The chart below shows that Google is down about 15% from its recent highs. Despite the recent market recovery, Google is lagging. This Justice Department case will likely weigh on the stock.

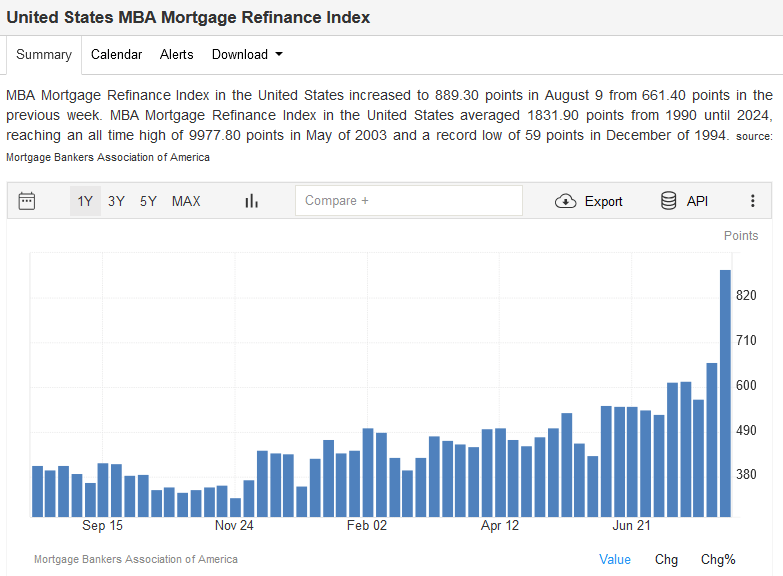

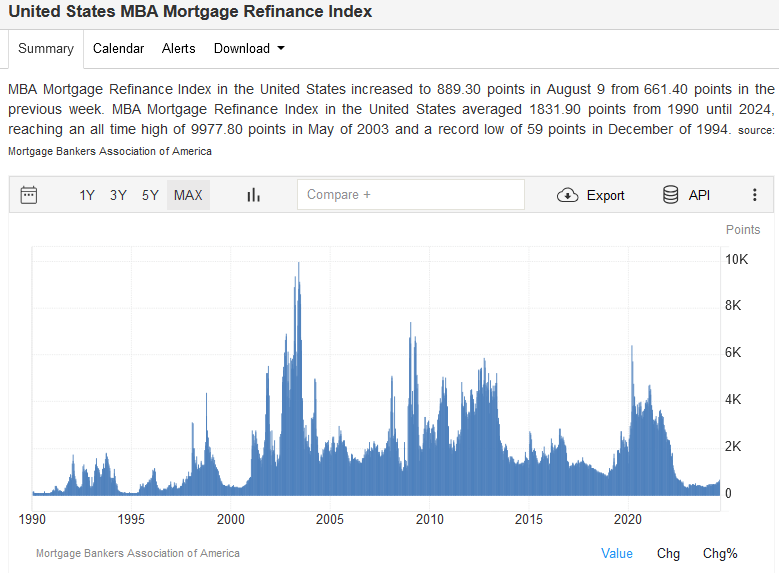

Mortgage refinancing is increasing, so to speak

The Fed attempts to control economic activity through its interest rate and QE policies. A critical aspect of its policies is their impact on housing markets. Low mortgage rates make it cheaper to buy a home and so can stimulate home sales, which in turn stimulate economic activity. Conversely, as we have seen recently, high mortgage rates restrict real estate trading.

A second aspect of Fed policy and its impact on mortgage rates is mortgage refinancing. When people refinance their mortgage into a new mortgage with a lower interest rate, they lower their interest costs. Therefore, they have more money to spend on other things. Over the last twenty years, mortgage refinancing has had a powerful economic effect.

With mortgage rates near 6.25%, nearly 2% below last year’s high, some mortgage borrowers who recently took out a mortgage will be incentivized to refinance their mortgages. The first chart below shows that the MBA mortgage refinance index has nearly tripled in the past year. While this may seem significant, a look at the longer-term chart shows that the index is still far from the average. In fact, it is still below the lows of the last 25 years. Since the number of homes sold in recent years has been below average, the number of potential refinances will also be below average. This means that the impact of a Fed rate cut on the mortgage refinance market will be much smaller than usual.

Tweet of the day

“Would you like to manage your portfolio more successfully in the long term? Here are our 15 trading rules for managing market risks.”

Please Subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to arrange a meeting.

Post views: 2

15.08.2024

> Back to all posts